May 2024 Monthly Review

"The Waiting Is The Hardest Part"

LJohnson@fcbanking.com

412-208-7687

Connect on LinkedIn

A Look Back

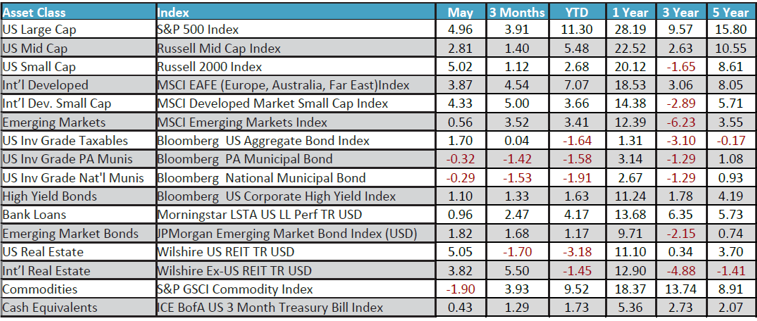

Tom Petty has never been more right. The single was released in 1981 and reached #1 on Billboards Rock Tracks chart. It was part of the Hard Promises album and remained at the top of the charts for six straight weeks in the summer of the same year. In an interview, Petty said that the song took a long time to write as, “I had the refrain down but had a hard time with the rest of the song.” He said it was about waiting for your dreams and not knowing if they will come true. I think just about everyone can relate to that sentiment at some point in their life and listening over the weekend got me thinking. We have been smack in the middle of one of the biggest waiting games in the financial markets that I can remember in my career, as extremely interested parties wonder if/when the Fed will start to cut short-term interest rates. The last rate hike occurred on July 27th, 2023. As we started 2024, the Fed Funds rate (the very short term rate that many money market rates are pegged to) stood at 5.25-5.50%, and the market expectations were that the rate would be cut five to six times in .25% increments throughout 2024. Guess what? It’s June, and we still stand at the same rate. With inflation being stubborn coming down, the Fed has been reluctant to reduce rates. The most recent PCE report showed core inflation rising .2% in April and 2.7% over the last year. That certainly is lower than the 4.7% number from April of 2023, but not the preferred 2% number the committee has been targeting and talking about. So, the waiting continues and the best bet now is for maybe one such cut this year with a real possibility of nothing happening as each economic release is analyzed and dissected. As we waited, stocks rebounded strongly in May. The S&P 500 rose by nearly 5%, while International equities had one of their best months of the year. Core bonds, which have languished in the uncertainty of rate cuts, bounced back as well with a 1.70% return, but are still negative so far this year. The latest U.S. employment report showed a lower than expected 175,000 jobs added in April, while the unemployment rate remained at 3.9%. Other major economic releases showed a slowing, but still growing economy for the most part. It is indeed a delicate dance that the Fed is trying to navigate…they have made it clear that they want strong, consistent evidence that inflation is under control before they switch gears and embark on a rate-cutting period, but higher-for-longer rates have a negative impact on businesses that depend on borrowing to finance their operations.

A Look Ahead

We have written often about the benefits of a longer-term view in the financial markets and the strength of a diversified asset allocation approach to investing. We take great comfort in what the historical numbers tell us and the real-life examples over time at just how resilient our markets have really been. All of that remains true, but it does not mean that we put up blinders in the short-term. In the end, our holy grail for our clients is always trying to deliver the most amount of return with the least amount of risk possible. With that in mind, we came into 2024 neutral in our allocation between stocks, bonds and cash. The stock and cash portions have served clients well, but bonds continue to disappoint. However, going forward, we do see a path forward where core bonds have a real chance to deliver outsized performance versus the historic norm. Maybe May was the start of that move, as we look for bonds to rally as yields across the curve come down. For now, like Tom Petty and even though it is hard…we wait.