January 2025 Monthly Review

"Here You Come Again"

LJohnson@fcbanking.com

412-208-7687

Connect on LinkedIn

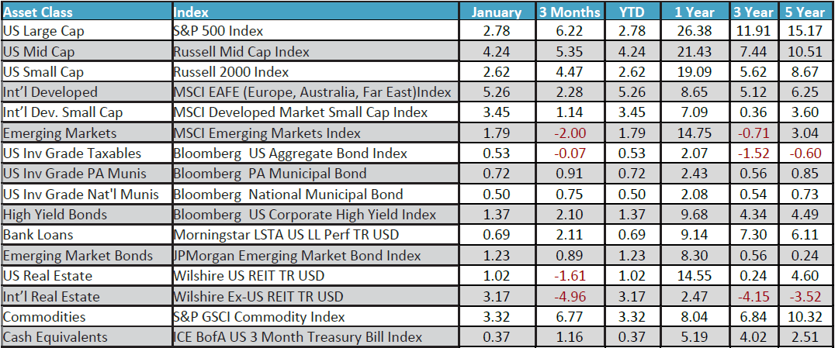

A Look Back

The above title was a hit by the great Dolly Parton. It was released in 1977, and topped the U.S. country singles chart for five weeks. It also reached #3 on the Billboard charts, marking Parton’s first significant pop crossover hit. I had not heard the song in years when it came across the radio recently, and it got me thinking about what has been going on in our country over the last few months…and particularly Donald Trump returning to the oval office after an improbable election win in November. January marked his official return and he wasted no time with a flurry of executive orders on a variety of fronts that included tariffs, immigration reform, regulations, etc. No matter your political affiliation, there seems to be little doubt that the 47th (and 45th) president intends to follow through on many of his campaign promises. Of course, in this venue, we are mostly concerned about how all of this may affect the financial markets. As always, we do look at the past for some guide to the future, and currently that view is a little murky. We definitely have seen some short-term volatility in the financial markets as they digest the various tariffs proposed and/or initiated against multiple countries. In addition, the surprising reduction in various government departments and agencies has increased the angst-level for those not used to such swift presidential action. Recent economic news has been at least okay for the most part. We added 143,000 jobs in January, a bit less than expected…but the unemployment rate ticked down to 4.0% from 4.1%. In December, the inflation gauge, CPI, rose .4%, bringing the full year number to 2.9%. This is still not where the Fed would like to see the number, and there are some signs that inflation will remain sticky for the near future…and maybe especially so if some of the proposed tariffs have the ultimate effect of raising prices here at home. With all that said, January started the year off right in all of the major indexes shown above. Large-cap U.S. stocks continued their strong run, up nearly 3%. Developed international stocks fared even better with a 5.26% return in the month. Core bonds delivered a return-to-normal return of .53%, which would imply around a 6% annualized number.

A Look Ahead

Generally speaking, as we meet with clients and prospects, even though we spend time discussing what has happened, we are most often asked what is going to happen. Financial markets have long humbled the brightest stars that believe they really have that question consistently figured out. We believe that a prudent level of remembering the past, along with a healthy dose of analyzing current conditions tends to be the best way to navigate the markets. Current U.S. big-cap stock valuations are stretched by almost any measure…and have been as we continue to press near all-time highs again. However, that means little in the short-run, as they can continue on that arc for quite some time. Additionally, earnings can surprise to the upside to bring those valuations back into line. As the new leadership takes hold, there is an optimism shared by many that policies may ultimately prove to be a good thing for the overall economy and the average consumer. How we get there, however, is not quite as clear. We are neutral in our stock allocation and believe it makes sense to have some downside protection on shorter-term money with valuations higher. Core bonds are likely to deliver more normal returns of 4-6% annualized. President Trump came again…and hopefully looking better than anybody has a right to...