April 2024 Monthly Review

"Did I Wait Too Long To Turn The Lights Back On?"

LJohnson@fcbanking.com

412-208-7687

Connect on LinkedIn

A Look Back

The actual title of the newest Billy Joel release is, “Turn the Lights Back On,” but the question above is the main question line in the chorus. I heard it for the first time recently as they celebrated Joel’s 100th performance at the Madison Square Garden in a TV special. It is a moving song with beautiful piano solos, and it examines a long-standing relationship that has apparently gone stale…and the singer wonders if it is too late to get back what they had in the past. It seems the lights had been turned off for some time.

It resonated, as we think about our economy and some of the decisions that our government or other appointed groups like the Federal Open Market Committee (FOMC or “the Fed”) make on a routine basis. Short-term interest rates and what the Fed has done with them over the last decade or so has been a big part of the market story over the same timeframe. They first took the Fed Funds rate to zero as a result of the Great Recession, and then again as a result of the Covid pandemic. Although totally different circumstances, in both cases the Fed was trying to do its part to respond to the crises and provide easy money to borrowers of capital…and ultimately help spur economic activity.

Fast-forward to the present, and the FOMC has gone the opposite way over the last couple of years…in an attempt to put the brakes on inflation specifically, and the economy to some degree. So, it’s a fair question: did they wait too late? Or, should they have waited later? We truthfully only know the answer to those types of questions years later, when we can look back with the benefit of tremendous hindsight. We have long said that we don’t love the idea of taking rates to zero, and especially leaving them there for extended periods. It creates some un-equal playing fields, and may not help the average wage-earner as much as Corporate America. We are dealing with the other end of the stick right now with higher interest rates that put burdens on those trying to borrow money or buy homes/cars etc.

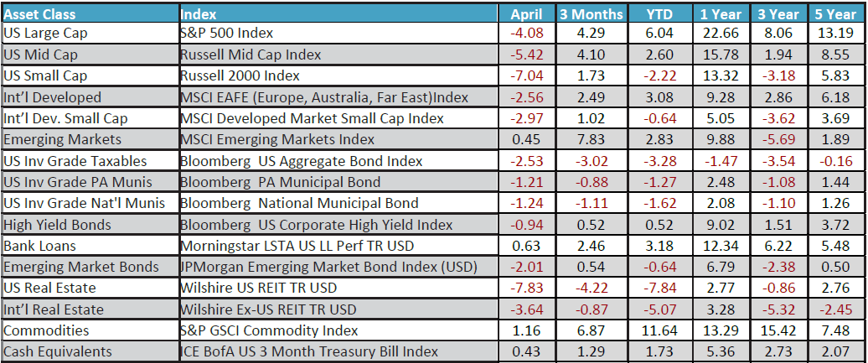

Like many things, the sweet spot is more in the middle…and in this case, maybe a Fed Funds rate of around 3% or so would do the trick. Financial markets struggled in April as it became clear that interest rate cuts were not in the immediate plans of the Fed as the latest reports showed inflation to be more sticky and problematic than hoped. The S&P 500 was down more than 4% in the month and core bonds continued their frustrating negative performance so far this year with a -2.53% return.

A Look Ahead

The Fed just met at the end of April and made it clear that rates were not heading down until they were more comfortable with inflation levels. Then, the April Jobs report just came out last week and showed the biggest disappointment and surprise in over two years. The unemployment rate climbed to 3.9% (still historically low) and only 175,000 jobs were added versus the expectations of over 240,000. However, in the world where bad news can be good news, it could be a sign that the economy is cooling down a bit…maybe the lag of the aggressive rate hikes is seeping in more and more, and the goldilocks soft/softer landing scenario is still attainable. Maybe. One report does not a trend make, so we will need to see more. With some renewed volatility in April, we still have not seen a one-day negative move of more than 2% in over 300 days. So, with inflation at 3.5% and U.S. personal savings down to 3.2% from 5.2% just a year ago, we remain cautious, as we trimmed stocks in early April, and wonder if the lights came on fast enough...