Quarterly Review and Outlook - March 2022

"If You Want a Guarantee, Buy a Toaster"

LJohnson@fcbanking.com

412-208-7687

Connect on LinkedIn

A Look Back

The above title was delivered by Clint Eastwood from the 1990 movie "The Rookie." The movie itself was never going to win an Oscar, but it did deliver a couple of memorable lines. Eastwood was paired with a young cop, played by Charlie Sheen, that didn’t exactly share his old-school way of looking at the world. When it was suggested by Sheen’s father that he wanted Eastwood to guarantee his son’s safety, Eastwood gruffly mumbled, “if you want a guarantee…buy a toaster.”

That line came to mind when talking about current markets with colleagues and peers. The first quarter of 2022 brought some volatility not seen since the beginning of the pandemic. The -4.60% drop in the S&P 500 was fairly routine, and not so unusual given the strong rally in 2020 and 2021.

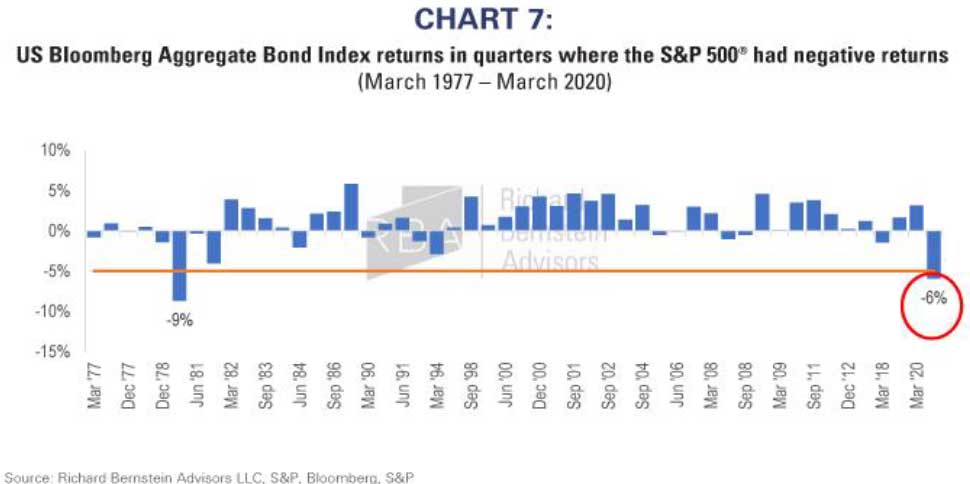

From the lows of March 2020, the broad stock index was up over 100%! What was much more unusual, and a bit of a sucker punch, was the negative return for the quarter in core bonds. As measured by the Bloomberg Aggregate, bonds were -5.93%. To put it in proper perspective, recall the chart we shared last quarter that showed the worst calendar-year return for core bonds was -2.92% in 1994. So, what is an investor to do? The two main components of most asset allocations, stocks and bonds, are down for the year…and the more “conservative” one (bonds) down more.

We do not believe all the things we have learned about market behavior and performance have suddenly gone out the window, but rather we are in the middle of several forces coming together at once that places stress on financial markets…and in some cases producing returns that take a moment to digest. In the same way that it would have been lunacy to predict a 70% rally from the lows of March 2020 into year-end, and an additional 29% in 2021, there is never that guarantee of how markets will behave…even when you think you know the news. The most recent reports showed inflation jumped 8.5% year-over-year, representing the biggest number since 1981. How the Fed plans to deal with that reality by raising short-term interest rates and selling assets from their balance sheet, dominated the headlines in the first quarter.

The same headlines continue to loom large in April. The Fed is attempting to engineer the so-called “soft landing” where they pump the brakes on inflation, while not braking too hard on the overall economy. Some also call this the “goldilocks” economy where inflation is not too hot and economic growth is not too cold. There is little doubt that manufacturing that perfect of an outcome is a difficult one. As mentioned, there are a variety of forces coming together at once that include a major military conflict with the Russian invasion of Ukraine, and the resulting worldwide fallout.

The chart below shows how rare the first quarter bond performance was. Historically, bonds have acted as a stabilizer to overall portfolio performance, and provided positive performance in the face of stock declines. Not so much in the first quarter of 2022. The aberration is big, but the one thing that we know in dealing with all asset classes over time is that outperformance tends to lead to underperformance and vice versa. All things being equal, we don’t believe core bonds should be abandoned as an asset class. We have been shorter than benchmark duration for some time now and favor some allocation into non-core asset classes like floating rate and short-term corporate, but at some point the higher coupons available in bond-land as a result of overall rising rates will be a good thing.

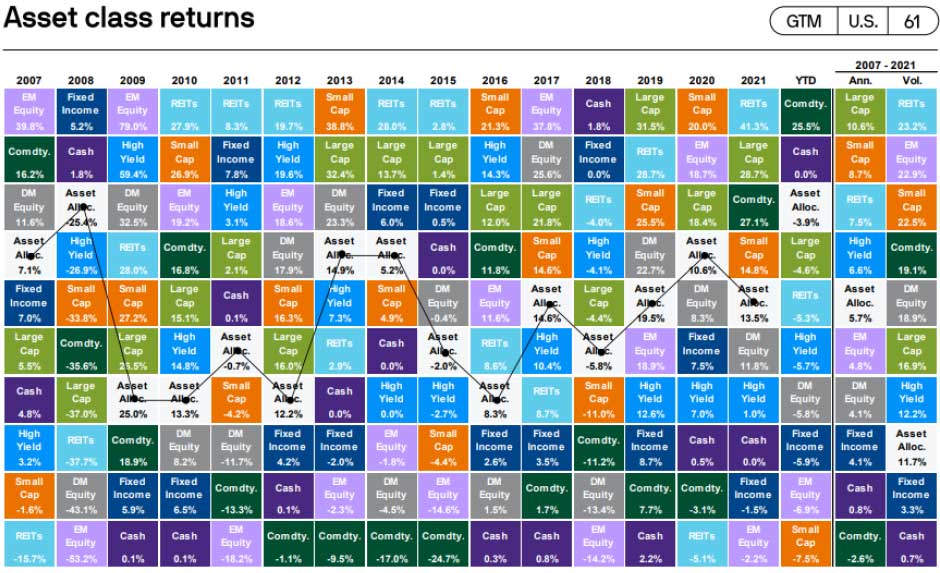

We include the chart below because nothing shows the fickleness of asset classes so vividly. Yesterday’s losers can, and usually do become tomorrow’s winners. Such has been the case with Commodities, which was the best performing asset class in the first quarter, up over 25%. We have been reminding clients over the last several months that cash, as unattractive as it is with yields between 0 and .2%, is still an asset class…and one worth holding when stocks and bonds are both struggling.

Importantly, the white box representing a typical 60/40 stock/bond allocation has generated an annualized return of 5.7% over the last 15 years. Those 15 years include the Great Recession timeframe of 2007-09 and the more recent Covid pandemic of 2020-present.

A Look Forward

It’s always difficult looking forward, and maybe even more so right now. Here are just a few of the concerns that have been lingering over markets over the last several months:

- Booming U.S. housing prices: home prices grew 17.1% in 2021 after a record increase of 18.4% in 2020.

- U.S. stock valuations near all-time highs at the start of 2022: CAPE ratio of 35, second only to dot.com era.

- Signs of speculative excesses: meme stocks like GameStop, AMC, Bed Bath & Beyond and others garner cult-like

following. IPOs and SPACs set records in 2021. SPACs have terrible history of performance once de-SPAC-ed. - Inflation as measured by CPI up 8.5%, the biggest number since 1981.

- Fed has announced not only an aggressive rate-hiking cycle that would currently take Fed Funds rate to 2.75% by

year-end, but plan on reducing size of balance sheet by $95 billion monthly going forward. (taper tantrum?) - Russia/Ukraine conflict leading to prolonged supply chain issues globally

However, there are positives to offset the dark clouds. Past crises tended to be caused by problems in the banking system. Today, banks are in much stronger financial positions, with better capital positions and tougher lending standards. The consumer has a much better balance sheet, with debt-to-income ratios at the lowest levels since 1980. Unemployment is at historically low levels, with initial jobless claims falling to a 54-year low of just 166,000. There are 1.8 job openings for each unemployed worker and the unemployment rate is at 3.6%. Finally, although the Fed has an incredibly tough task ahead, they have been fairly transparent in what their thinking is.

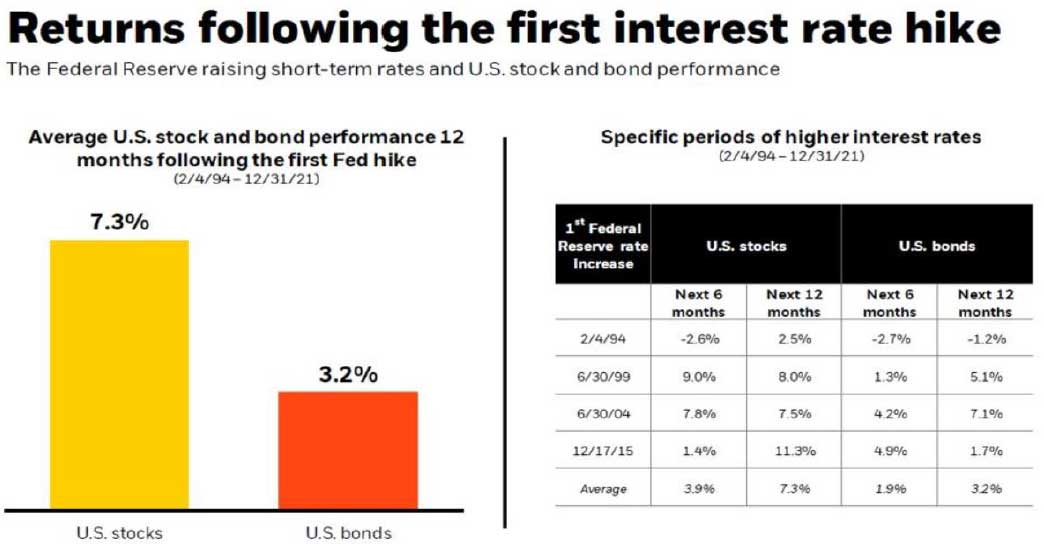

In the end, markets hate uncertainty, so to the extent that they maintain this approach, it gives them a fighting chance to realize the goldilocks ending. The table above shows how stocks and bonds have performed in the last four rate-hiking periods. A year later, stocks were up an average of 7.3%, while bonds were positive by 3.2%. Clint had it right: no guarantees, but we will stick to what we know works over time by employing a thoughtful, diversified, managed portfolio…taking advantage of opportunities as they present themselves